Download PDF

Download PDF- Demographics, debt and disruptions are often the main deflationary culprits, but we think the American household has been responsible for the slowdown in global borrowing and spending.

- The Chinese economy has been the most acutely affected by the collapse in U.S. household credit demand.

- Unless another major global spender comes along, the Federal Reserve could be done with tightening for the next decade.

“...don’t think rates will rise…maybe never again in my lifetime.”

-Larry Kudlow, Director of the National Economic Council during an interview on April 11, 2019White House National Economic Council Director Larry Kudlow is 71. The life expectancy of the average 71-year-old American male is an additional 13.7 years based on the 2016 period life tables published by the U.S. Department of Social Security. So Kudlow’s forecast is a bold one, assuming his life expectancy is the average. He is saying we are not even halfway through the historic period of rock bottom interest rates that has developed since the Great Financial Crisis (GFC).

Change Since The GFC

This blog is about why he might be right. The usual arguments that come up in this discussion are the deflationary “Ds”: demographics, debt and the disruptions coming from globalization, technology and competition. The “Ds” all support Kudlow’s case. But my focus here is to show why Kudlow’s forecast is strengthened by a key macro regime shift that has been and remains in play since the GFC.

Much of the research on the cause of the GFC has centered on the lack of regulatory oversight and the build-up of financial system risk. It ultimately resolved with a near-collapse of the system itself. But the recession that followed the GFC and the weak global expansion that has unfolded over the last 10 years has to do with other factors. The main culprit has been a major slowdown in borrowing and spending in the global economy on the part of the world’s most important private sector spender and source of aggregate demand: namely, the American household.

Americans Become Savers

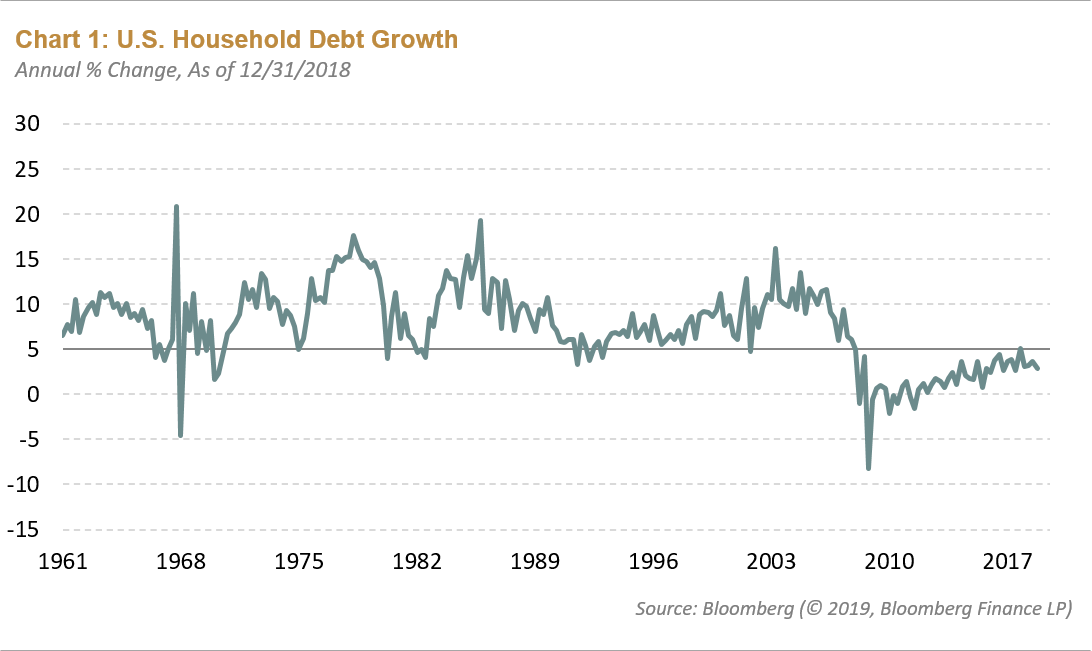

For decades American household borrowing ran faster than income creation, driving household leverage up and the personal savings rate down. The perpetual cycle of borrowing helped prop up spending and inflated economic growth—a phenomena that Tony Boeckh, my former colleague and mentor at BCA Research, was the first to describe as The Super Cycle of Debt. During my years at BCA we wrote constantly about the sustainability of this debt cycle and worried what would happen when it came to an end. Chart 1 shows that the growth rate in household credit never retreated significantly below 4-5% at any time from 1946 right up to 2008—a relentless buildup in household leverage for six decades. It all finally ended in 2008 with the GFC.

Household credit collapsed to a -10% growth rate during 2008. The contraction did not stop for another four years after the GFC. Still today, household credit is barely rising at 2.9%, well below nominal income and gross domestic product (GDP) growth rates and well below any experience of the 60 years before the GFC. The shock of the GFC catalyzed a decision among households to stop borrowing, start saving, and to de-lever. For Baby Boomers it was time to start saving for retirement after a decade which saw two 50%+ swoons in the stock market and a once-in-a lifetime real estate bust. Born minimalists, Millennial spending and borrowing remains underwhelming. Household debt-to-GDP has dropped 20 points from its peak of 100% in 2007. Had this ratio sustained its 2007 peak for the last 10 years, there would have been over $6 trillion more in household credit creation—$600 billion more per year—another 3.5% annual credit growth, and a lot more spending.

The impact of the collapse in U.S. private credit demand is very evident in inflation-adjusted U.S. bond yields. The 10-year real yield fell from a pre-crisis level of roughly 2.25% and bottomed out at -80 basis points (bps) in late 2012 as credit stopped contracting. Since then, real yields stabilized around 50 basis points—as credit growth creeped back above zero—before briefly piercing 100 bps last year.

China Gears Up

But real yields reflect the intersection of the global demand and supply of credit. The largest economy most directly affected by the collapse in U.S. household credit demand has been China. China’s ascendance during the 20 years prior to the GFC took place on the back of the massive savings surplus it was able to recirculate through the American spending and borrowing cycle. For decades it was a win-win relationship: U.S. consumers borrowed and binged on a steady inflow of low-cost Chinese imports with American debt vendor-financed by Chinese savers. The result was a steady side-by-side increase in U.S. household leverage and Chinese economic growth.

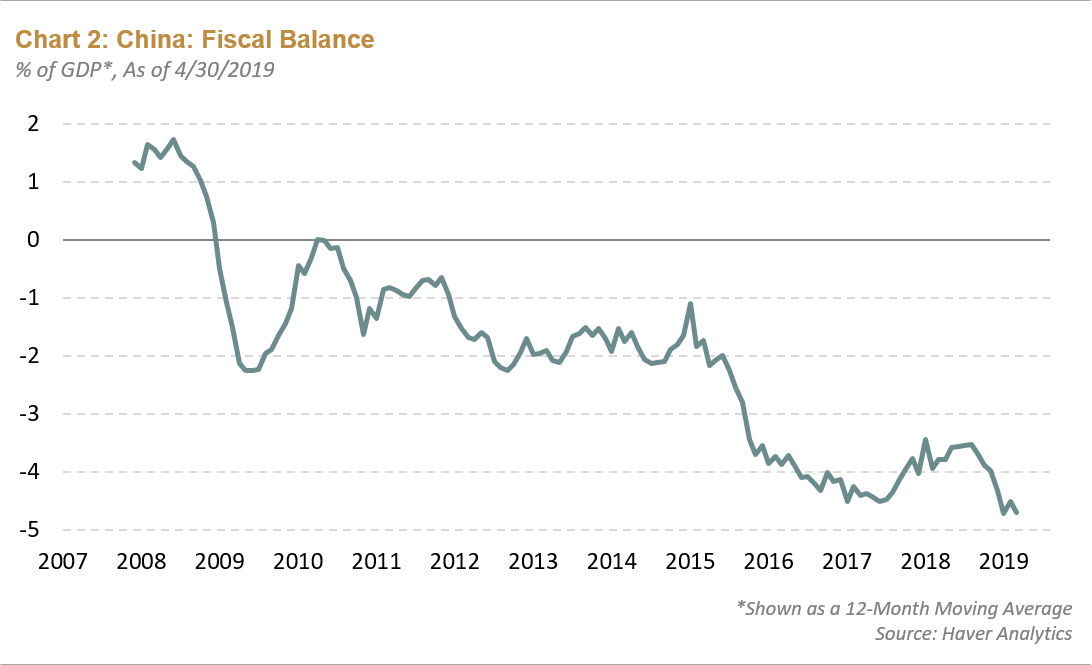

The Chinese government had few options when U.S. household borrowing finally caved in. Beginning in 2009, China aggressively boosted fiscal policy and total social financing to stave off a domestic cycle of over-production and deflation. After 10 years, China’s efforts to offset the effects of U.S. household deleveraging by spending domestically has left the economy over-leveraged and with a central government budget deficit of almost 5% of GDP (see Chart 2), and closer to 11% of GDP if all levels of Chinese government are considered. In the meantime, the U.S. budget deficit has risen to 6-7% of GDP owing to the Trump Tax Cuts. Despite these large budget deficits in the world’s two most important economies and 10 years of economic expansion, Japanese and German bond yields are at zero, 10-year Treasurys are 2.5%, and the yield curve is flat.

Any Big Spenders Left?

The only way this story changes is if another big spender comes along. But the two biggest contenders are already tapped out. In the U.S., the Senate won’t entertain an infrastructure plan without financing details. In China, policy leaders don’t want to keep gearing up the economy. As for the private sector, large population groups in the developed countries are shrinking and China’s cresting supply of labor means it could get old before getting rich. There is always a chance that corporate spending fills the void but so far that has not happened.

Therefore, it looks like the big dis-savers are done spending for now and we are entering a new phase where old ideas resurface like the Modern Monetary Theory (MMT), which asserts that governments should just keep spending and central banks finance directly to prop up nominal growth. Parts of the world have already been doing this. The only difference is the half step of government debt issuance which the central banks of Japan and Europe have been buying; that has not been the case in the U.S., at least not yet. So, Kudlow could be right. The Federal Reserve might be done tightening for the next 10 years.

Groupthink is bad, especially at investment management firms. Brandywine Global therefore takes special care to ensure our corporate culture and investment processes support the articulation of diverse viewpoints. This blog is no different. The opinions expressed by our bloggers may sometimes challenge active positioning within one or more of our strategies. Each blogger represents one market view amongst many expressed at Brandywine Global. Although individual opinions will differ, our investment process and macro outlook will remain driven by a team approach.