Download PDF

Download PDF

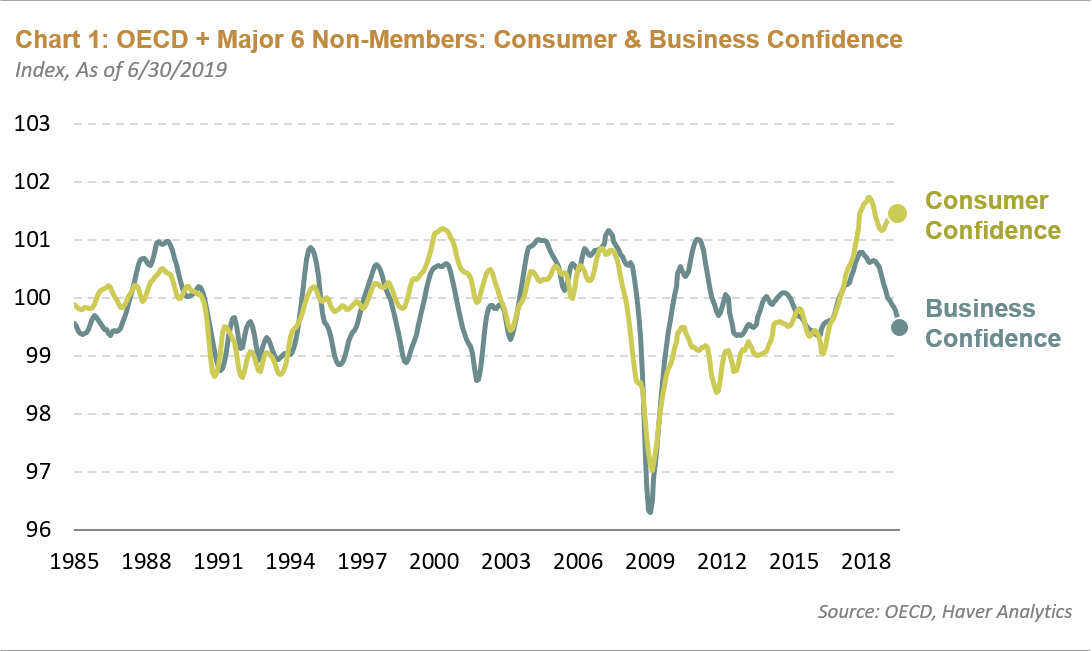

While the global economy hasn't recently experienced a huge shock to the system like it did in '98 or '10, the slowdown in Chinese economic growth has weighed on business confidence. We have seen other related measures such as capital expenditures (capex), Purchasing Manager Indices (PMIs), inventories, and export orders all weaken as well. So what's driving this dichotomy between businesses and consumers?

Globally, consumers still have reasons to remain optimistic: unemployment rates are low while wages are up. Retail sales have remained buoyant, a signal we think confirms this positive sentiment. Interestingly, small business confidence also remains high in the U.S., which means domestic conditions are more buoyant relative to global economic activity and global trade flows. It's therefore the management teams of multinational companies that are pessimistic; U.S. CEO surveys also reflect this development. The virtuous cycle created by consumers has been pitted against a vicious one resulting from negative business sentiment. Which one will win out? We will be watching domestic demand-driven economies closely to see whether these positive domestic factors put upward pressure on business confidence. Any positive news on the U.S.-China trade negotiations should also perhaps change business sentiment—which doesn't appear likely over the near term. Regardless, we don't think this divergence will be sustainable in the long run. However, one of them will reach an inflection point in the intermediate term.

This divergence has not gone unnoticed by central banks and has continued to confound monetary authorities. Aside from persistently low inflation, global central banks will be tasked with addressing these conflicting sentiment factors over the course of the next year. Can central banks be nimble enough to react to the upcoming convergence in sentiment? Time will tell.

Groupthink is bad, especially at investment management firms. Brandywine Global therefore takes special care to ensure our corporate culture and investment processes support the articulation of diverse viewpoints. This blog is no different. The opinions expressed by our bloggers may sometimes challenge active positioning within one or more of our strategies. Each blogger represents one market view amongst many expressed at Brandywine Global. Although individual opinions will differ, our investment process and macro outlook will remain driven by a team approach.